Explore affordable term insurance for women in the UAE. Learn about benefits, best plans, eligibility, and how to choose the right coverage to protect your family.

Term Insurance with Return of Premium

4.6/5

26316

35+

Insurance Partners

1.5 Million+

Trusted Customers

750 K+

Policies Sold

AED 1 Million Cover

Starting @ AED 50/month*

Monthly Income (Dirhams)

1k - 3k

3k - 5k

5k - 8k

8k - 10k

10k - 15k

15k - 20k

20k+

Term insurance is a type of life insurance that provides coverage for a specified period, ensuring financial security for the beneficiaries in the event of the policyholder's demise during the policy term.

While term insurance is gaining popularity in the UAE due to its straightforward nature and affordable premiums, several individuals hesitate to invest as they won't receive any survival benefits if they outlive the policy.

Addressing this concern, some prominent insurers have introduced term insurance plans with return of premium options. Essentially, this means that if you're alive at the end of the policy term, all the premiums paid are returned to you.

Table of Content

This article dives deeper into the nuances of term insurance with return of premium, shedding light on its features, benefits, and why it might be the right choice for those looking for the best of both worlds.

What is Term Insurance with Return of Premium?

At its core, term insurance is designed to offer life coverage for a predetermined duration. If the policyholder passes away within this term, a death benefit is given to the beneficiaries. However, if the policyholder survives the term, no benefits are typically provided.

This is where the ‘return of premium’ feature comes in.

Term insurance with return of premium, often abbreviated as TROP, is a special type of term insurance plan. In a TROP plan, if the policyholder outlives the policy term, the insurance company returns all the premiums that were paid throughout the tenure.

This feature is similar to getting a refund for not making a claim. It addresses the common concern that many have about supposedly ‘wasting’ money on insurance if they outlive the term. With TROP, policyholders can have peace of mind knowing that they either get protection for their loved ones or their money back at the policy's end.

How Does Term Insurance Plan with Return of Premium Work?

To understand how a term insurance plan with return of premium (TROP) works, it's essential first to distinguish it from a basic term insurance plan.

Basic Term Insurance

A standard term insurance policy provides life coverage for a certain period or term. If the policyholder, let's call him Ahmed, passes away within this term, his beneficiaries receive a death benefit. This benefit is a predetermined amount of money and ensures that Ahmed's loved ones have financial security in his absence.

However, if Ahmed outlives the policy term, neither Ahmed nor his beneficiaries receive any benefits or returns from the premiums paid. This is because his plan is a pure protection one.

Term Insurance with Return of Premium

Let's now introduce the TROP feature. In this plan, the policy works similarly to the basic term insurance for the duration of the policy term. If the policyholder dies during the term, the beneficiaries get the death benefit.

The significant distinction here becomes apparent if the policyholder survives the term. Instead of the premiums simply being an expense for the peace of mind, they are returned to the policyholder at the end of the policy term.

In essence, it's like a money-back guarantee for outliving the policy.

Example

Let's consider a UAE resident called Abdul. He opts for a TROP term insurance plan with a term of 20 years, paying an annual premium of AED 10,000. If Abdul were to sadly pass away within these 20 years, his family would receive the agreed-upon death benefit, ensuring they're financially stable during such a challenging time.

However, if Abdul survives these 20 years, he will receive back all the premiums he paid over the years. In this scenario, Abdul would get around AED 200,000 (AED 10,000 x 20) at the end of the policy term.

In essence, while basic term insurance offers peace of mind with its death benefit, term insurance with return of premium goes a step further. It provides both the security of a death benefit and the assurance of returned premiums if the policyholder outlives the term.

Best Term Insurance Plans with Return of Premium

Let’s take a look at some of the best term insurance plans with return of premium along with their some key details in the table below:

| Term Insurance Plans with Return of Premium | Sum Assured | Entry Age | Maximum Maturity Age |

|---|---|---|---|

| SBI Life Smart Swadhan Plus | 20 lakhs to 10 crores | 18 to 65 years | 70 years |

| Aditya Birla Capital DigiShield Plan |

|

18 to 65 years | 85 years |

| ICICI iProtect Return of Premium | 25 lakhs to 20 crores | 18 to 60 years | 85 years |

| Max Life Return of Premium | 25 lakhs to 10 crores | 18 to 65 years | 82 years |

| HDFC Click 2 Protect Super | 25 lakhs to 5 crores | 18 to 65 years | 85 years |

| Tata AIA SRS Vitality Protect | 50 lakhs to 5 crores | 18 to 60 years | 85 years |

| Canara HSBC Young Term Plan Life Secure TROP | 25 lakhs to 20 crores | 18 to 45 years | 99 years |

| PNB MetLife Mera Term Plan Plus | 50 lakhs to 1.5 crores | 18 to 50 years | 80 years |

Key Benefits of Term Insurance Plan with Return of Premium

Term insurance with return of premium offers a unique blend of protection and savings. While its primary goal is to safeguard one's family in unforeseen circumstances, the TROP feature ensures that the policyholder's investment isn't lost if they survive the term.

Let's discuss the key benefits of this insurance variant -

- Comprehensive Coverage: Term insurance with return of premium (TROP) provides complete life coverage, ensuring beneficiaries receive a substantial death benefit in the event of the policyholder's demise.

- Guaranteed Return of Premium: If the policyholder outlives the term, they receive back all the premiums paid, making it a financially prudent choice.

- Maturity Benefits: Beyond just the returned premium, some TROP plans may also offer additional maturity benefits or bonuses, which further increases the total payout.

- Flexible Premium Payment Options: Policyholders can choose how they wish to pay the premiums: as a single lump sum, annually, half-yearly, or even monthly, suiting their financial convenience.

- Shield Against Uncertainty: In volatile times, this type of insurance ensures that loved ones remain financially secure regardless of unforeseen events.

- Retirement Financial Support: The returned premiums can serve as a substantial savings cushion, especially helpful during retirement years when regular income may decrease.

- Peace of Mind: With both protection and guaranteed returns, policyholders can have peace of mind knowing that their investments serve dual purposes.

Drawbacks of Term Insurance Plan with Return of Premium

While term insurance with return of premium offers numerous advantages, it also comes with its own set of drawbacks like any other financial product. It's crucial for potential policyholders to be aware of these challenges to make an informed decision.

Here are some of the limitations associated with term insurance with return of premium:

- Higher Premiums: The most noticeable downside is the cost. Premiums for TROP term plans are typically higher than standard term insurance. While policyholders do receive their premiums back if they outlive the term, they pay a premium for that feature during the policy's tenure.

- Potential Opportunity Cost: The extra money spent on the higher premiums could potentially be invested elsewhere for potentially higher returns. Simply put, there might be better investment avenues that offer more attractive returns over the same duration.

- Not a Pure Investment Vehicle: TROP might give back the premiums but it doesn't offer the growth potential associated with other investment tools like mutual funds or stocks. For those looking for an investment-first approach, TROP might not be the best fit.

- Longer Commitment: TROP plans usually require a longer commitment. This extended duration might not be suitable for everyone, especially if they want the flexibility to shift their financial strategies.

- Limited Flexibility in Policy Changes: Making changes or adjustments to a TROP policy might be more challenging compared to regular term policies. Certain modifications could result in losing the TROP feature or incurring additional fees.

Who Should Buy a Term Insurance Plan with Return of Premium?

Term insurance with return of premium offers a distinctive combination of protection and savings.

But is it right for everyone?

Well, the decision to invest in this type of policy often depends on an individual's specific life situation, financial needs, and future goals.

Let's explore who might benefit the most from TROP and why:

-

Single Individuals

- Future Planning: Even if they currently have no dependents, single persons might want to lock in a lower rate now, anticipating future family responsibilities. As TROP ensures the return of premiums, it offers both protection for potential future dependents and a savings mechanism.

- Financial Flexibility: For those who are cautious about losing their money in term insurance, TROP offers a way to secure life coverage while still retrieving the premiums at the end of the term.

-

Married People with No Kids

- Partner's Security: In the event of an untimely death, the policy ensures that the surviving spouse has financial stability.

- Shared Financial Goals: As the couple plans for shared long-term goals, the return of premiums can be a welcome addition to their financial planning, perhaps going towards a significant joint expense.

-

Married Individuals with Kids

- Children's Welfare: Beyond just their partner, these individuals now have the added responsibility of securing their children's future. This policy ensures the family's financial security.

- Educational and Life Goals: The returned premiums at the end of the term can be set aside for children's higher education or other significant milestones.

-

Individuals Seeking Savings Discipline

- Structured Savings: Paying regular premiums enforces a discipline of savings, while the guaranteed return ensures the money isn't lost.

- Future Financial Cushion: The lump sum received at the end of the term can act as a significant financial boost for future needs.

-

Those Hesitant About Traditional Term Insurance

- Perceived Value: For individuals who perceive traditional term insurance as a potential loss if they outlive the policy, TROP provides an alternative where they can secure coverage without the fear of losing money.

How to Choose a Term Insurance Plan with Return of Premium Benefit?

Navigating the myriad of insurance options can seem overwhelming, especially when considering the added layer of the return of premium (TROP) benefit. The allure of getting back what you pay is undoubtedly attractive, but how do you ensure you're picking the right plan that suits your requirements?

Here are some crucial factors to consider when choosing a term insurance plan with return of premium -

-

Cover Amount

- Assessment of Requirements: Start by evaluating your financial liabilities, future expenses, and the lifestyle that you wish to secure for your loved ones. This will help you determine the suitable coverage amount.

- Future Projections: Remember to account for inflation and potential life changes such as marriage, childbirth, or purchasing a home, all of which can impact the required coverage amount.

-

Premium Amount

- Budget Compatibility: While TROP plans are enticing with their return promise, they come at a higher premium than standard term plans. Make sure the premium is manageable within your budget without straining your regular expenses.

- Compare Across Providers: Shop around and compare premium amounts across different insurance providers to get the best value for your money.

-

Claim Settlement Ratio of the Insurer

- Track Record: This ratio indicates the number of claims settled by the insurer against the total claims received. A higher ratio suggests a better track record, instilling confidence that your claim (or your beneficiaries' claim) will be honoured.

- Reliability: Opting for an insurer with a good claim settlement ratio ensures that the main objective of the insurance – beneficiary support in the policyholder’s absence – is met without hassle.

-

Policy Tenure and Flexibility

- Duration: Check whether the policy duration aligns with your long-term financial goals and retirement age. If you're aiming to use the returned premium as a retirement corpus, align the policy's maturity with your retirement age.

- Adjustment Options: As life is unpredictable, it’s advisable to choose a policy that offers some degree of flexibility. This might include allowing you to increase the cover amount during significant life events like marriage or childbirth.

-

Additional Riders or Benefits

- Enhanced Protection: Some insurance providers may offer additional riders like critical illness cover or accidental disability benefits at an extra cost. Depending on your health and lifestyle, consider if these additional benefits would be advantageous for you.

Over to You

Term insurance with return of premium (TROP) stands out as a unique and valuable option in the landscape of life insurance offerings. By providing the protective qualities of standard term insurance with the added allure of receiving all your premiums back on outliving the policy term, TROP has carved out a niche for those who value both security and the promise of a return.

With that said, like all financial decisions, choosing to invest in TROP should be approached with prudence. It's essential to recognise that while this plan addresses the hesitancy some may feel about traditional term insurance, it comes with its own set of considerations, especially in terms of higher premiums.

Individuals must weigh the peace of mind this policy brings against the higher costs and potential returns from other investment avenues.

Policybazaar Insurance UAE – Helping you navigate the wilderness of the insurance world!

More From Term Insurance

Recents ArticlesPopular Articles

Term Insurance for Women in the UAE

Term Insurance for Women in the UAE Life Insurance for Parents in UAE

Life Insurance for Parents in UAELooking to secure your parents’ financial future? Explore life insurance for parents in the UAE, including benefits, types, how to apply, and what to consider when choosing a plan.

Best Term Insurance Plans for Self-Employed in UAE – Secure Your Future

Best Term Insurance Plans for Self-Employed in UAE – Secure Your FutureExplore the best term insurance plans for self-employed individuals in the UAE. Get financial security for your family & business with affordable coverage options. Compare & apply now.

Zurich Futura Whole Life Insurance – Benefits, Features & Coverage in UAE

Zurich Futura Whole Life Insurance – Benefits, Features & Coverage in UAEDiscover Zurich Futura Whole Life Insurance in the UAE. Get lifelong coverage, flexible benefits, and investment growth. Learn about policy features, optional riders, and how to apply today!

Best Life Insurance Companies in the UAE – Compare & Choose the Right Policy

Best Life Insurance Companies in the UAE – Compare & Choose the Right PolicyLooking for the best life insurance companies in the UAE? Compare top insurers, coverage options, and claim settlement ratios to secure your family’s financial future.

Term vs Whole Life Insurance in UAE: Key Differences & Benefits

Term vs Whole Life Insurance in UAE: Key Differences & BenefitsCompare term and whole life insurance in the UAE. Understand key differences, benefits, costs, and which plan suits your financial goals and budget.

- Sum Insured vs Sum Assured: Key Differences & Insurance Guide

Understand the difference between sum insured vs sum assured in insurance. Learn about their meanings, key features, and how to choose the right coverage for your needs.

Takaful Emarat Life Insurance | Choose Best Takaful Emarat Life Insurance in UAE

Takaful Emarat Life Insurance | Choose Best Takaful Emarat Life Insurance in UAETakaful Emarat Life Insurance UAE - Compare & Buy Takaful Emarat Life Insurance in Dubai, UAE. Get Financial assurance for your family with a Takaful Emarat Life Insurance

Why Choose Twenty Five Year Term Life Insurance?

Why Choose Twenty Five Year Term Life Insurance?In this article, we will understand all the key details about 25 year term insurance and its usefulness.

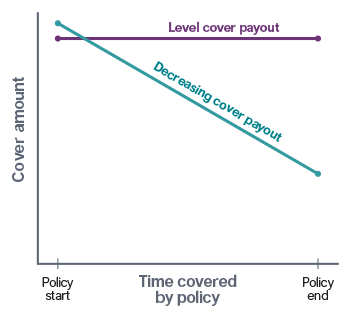

Level or Decreasing Life Insurance: What's the Difference?

Level or Decreasing Life Insurance: What's the Difference?In this article, we will explore the distinction between decreasing vs level insurance, the benefits of each type, and how you can determine what works best for you.

All You Need to Know About Level Term Life Insurance in UAE

All You Need to Know About Level Term Life Insurance in UAELet’s discuss the distinctive properties of level term insurance and its benefits. We will also understand the level term life insurance rates so that you make an informed decision!

- 10 Crore Life Insurance Policy - A Complete Guide

A 10 crore life insurance policy offers extensive coverage. It ensures the financial well-being of the family and allows them to maintain their lifestyle and meet their financial goals even in the policyholder’s absence.

- What is Surrender Value in Insurance?

Surrender value in insurance is the amount of money a policyholder receives if they cancel their policy before it matures. Check two main types of surrender values - Guaranteed Surrender Value and Special Surrender Value.

- Term Insurance Premium Calculator - A Complete Guide

Term insurance premium calculator in the UAE offers numerous advantages, streamlining the process of selecting the most suitable term insurance plan.

Who Should Be Your Nominee for Your Term Insurance?

Who Should Be Your Nominee for Your Term Insurance?We will explore into the nuances of term insurance, elucidating the meaning of the insurance nominee meaning, life insurance nominee rules, and much more.

Understanding the Slide of Decreasing Term Insurance

Understanding the Slide of Decreasing Term InsuranceWe will explore the nuances of the decreasing term life insurance plan, highlighting its salient features, benefits, and more.

Deciphering the Pros and Cons of a Term Insurance Policy

Deciphering the Pros and Cons of a Term Insurance PolicyDiscover the reasons to consider a term insurance policy. This guide provides all the information you need to make an informed decision.

How Important Is Term Insurance for Non-Working Spouses in India?

How Important Is Term Insurance for Non-Working Spouses in India?If you're married and your spouse doesn't work, explore the responsibilities and contributions of a non-working spouse, while often underestimated, are foundational to a household's functioning.

Why is Medical Test Important in Term Insurance?

Why is Medical Test Important in Term Insurance?Learn about the importance of medical tests and find out if they're covered by your policy. Protect yourself and your loved ones with term insurance.