Explore the best term insurance plans for self-employed individuals in the UAE. Get financial security for your family & business with affordable coverage options. Compare & apply now.

Why is Medical Test Important in Term Insurance?

4.6/5

25476

50+

Insurance Partners

1 Million+

Trusted Customers

250 K+

Policies Sold

AED 1 Million Cover

Starting @ AED 50/month*

Monthly Income (Dirhams)

1k - 3k

3k - 5k

5k - 8k

8k - 10k

10k - 15k

15k - 20k

20k+

Why is a medical test so pivotal in the process of obtaining term insurance? If you're considering the path of ensuring the financial security of your loved ones, term insurance is undoubtedly one of the smartest decisions you can make.

However, there's a vital step involved before you can purchase this safeguard: a series of medical tests. These tests, far from being a mere formality, play a quintessential role in determining your health status.

This can immediately lead to a few related questions — What happens if you fail the term insurance medical test? How does it influence the policy's premiums and terms?

Table of Content

The article below will offer you an all-encompassing guide about these medical tests and the related queries so that you're well-equipped to navigate the intricacies of buying term plans.

Importance of Medical Tests in Term Insurance

While term insurance serves as a crucial financial buffer for your family's future, the underpinning principle of such policies is the assessment of the risk associated with insuring an individual. This is where medical tests come into play.

Primarily carried out to ascertain the customer’s health risk, these examinations play a pivotal role in the insurance domain.

Let’s take a look at the basics of how these tests influence term insurance -

- For Deciding Premium Amount: Medical tests are instrumental in determining the premium that you will pay for your term insurance.

For instance, a 40-year-old individual with a history of diabetes and high blood pressure might have to pay a premium of AED 2,000 annually, while a healthy counterpart of the same age could be quoted AED 1,200. The difference stems from the perceived higher risk of mortality in the former case.

- To Offer an Assured Sum: The results of the medical tests also help insurance companies decide the sum assured. A person with a clean bill of health is often eligible for a higher assured sum at a lower premium.

So, if Mr. Ahmed, a non-smoker with no underlying health conditions, seeks a policy, he might be offered an assured sum of AED 1 million. On the other hand, Mr. Rashid, a smoker with mild respiratory issues, might only be eligible for AED 700,000.

- Claim Settlement and Rejections: An accurate representation of health status backed by medical tests is pivotal during claim settlements. For instance, if a policyholder makes a claim for a critical illness benefit, the medical tests prior can serve as a baseline for the insurance company to ascertain the validity of the claim. Moreover, if any discrepancies arise between the actual health condition and the declarations made during policy purchase, it can lead to claim rejections.

A scenario could be Mrs. Fatima, who did not disclose her pre-existing heart condition and unfortunately passed away due to a heart-related ailment. In this case, her family might face challenges in getting the claim settled.

Who Needs to Undertake Medical Tests for Term Insurance?

The journey of obtaining term insurance often leads prospective policyholders to the doorstep of medical evaluations. But does everyone need to cross this threshold? Interestingly, whether or not one has to undertake a medical test often varies based on several factors.

Here's how the decision branches out based on the type of term plan:

- Pre-written Term Plans: This is essentially an off-the-shelf insurance product, where the policy's sum assured has a predefined limit. Those who opt for this kind of policy usually don't need to undergo medical tests. Instead, the policy issuance relies heavily on the applicant's health declaration. If a policyholder vouches for being in good health and meets the other criteria, the insurance plan is granted without additional health evaluations.

- Underwritten Term Plans: In contrast to pre-written plans, underwritten ones involve a more detailed assessment. The requirement for medical tests here primarily hinges on two pivotal factors: the desired sum assured and the applicant's age.

Example

Consider Mr. Abdullah, aged 35, who wants to obtain a term plan with a sum cover of AED 1 million. Being younger and within this coverage limit, his policy might be classified as a Non-medical case. This means the policy would be issued based on his health declaration alone, provided he doesn't disclose any concerning health conditions.

Conversely, Mr. Hussain, aged 50, aiming for the same coverage, will find himself on a different trajectory. Given his age bracket, even if he's eyeing the same sum cover as Mr. Abdullah, he'll likely need to undergo medical tests. However, these tests might not be exhaustive — they could be as basic as a Medical Examination Report (MER) and a lipid profile.

In essence, while the type of term plan — be it pre-written or underwritten — sets the initial direction, age and desired coverage play pivotal roles in determining whether medical evaluations are essential. This structured approach ensures that each policyholder receives coverage that's in sync with their unique profile, striking a balance between convenience and comprehensive assessment.

Medical Tests Required for Term Insurance

When opting for term insurance, it's crucial to understand the array of medical tests that might be on the horizon. Each test delves into different facets of your health, ultimately assisting insurers in gauging your risk profile.

Here's a comprehensive rundown of these tests and their significance:

| Test/Examination | Purpose and Assessment |

|---|---|

| Medical Examination Report | This general physical examination offers a holistic view of an individual's current health status. It covers aspects like height, weight, blood pressure, and the identification of any noticeable ailments. |

| Urine Cotinine | Primarily used to detect nicotine presence, this test helps in verifying whether the individual is a smoker or uses tobacco products. These habits can lead to a higher premium due to increased health risks. |

| Exercise ECG Bruce Control | A type of stress test, it monitors how your heart responds to exertion. It can help identify irregular heart rhythms or highlight potential coronary artery diseases. |

| Microscopic Urinalysis | By examining a urine sample under a microscope, this test checks for signs of kidney disease, diabetes, or urinary tract infections, among other conditions. |

| PSA (Prostate Specific Antigen) | Specifically for men, this test gauges the level of PSA in the blood. Elevated levels might indicate prostate issues, including potential cancer. |

| HbA1c and Total Cholesterol | HbA1c measures average blood sugar over the past 2-3 months, pointing towards diabetes control. Total cholesterol, on the other hand, offers insights into heart health and the potential risks of cardiovascular diseases. |

| Lipid Profile and HbA1c | The lipid profile breaks down the types of fats in your blood for a perspective on your heart’s health. When combined with HbA1c, it offers a dual view of cardiovascular and diabetic risks. |

| Complete Blood Count, Gamma GT, AST, Creatinine, and ALT | This suite of tests evaluates overall health by studying blood components, liver function (Gamma GT, AST, ALT), and kidney function (creatinine). Any anomalies can signal potential health issues that might influence the insurance premium. |

Disclaimer: The tests mentioned above serve as a general guideline. Depending on your insurance provider, the requirements and specifics of the medical tests may change.

What If I Fail Medical Test for Term Insurance?

The potential outcomes of medical tests for term insurance are given below –

- Acceptance as a Standard Case: This is the ideal scenario. After you undergo medical tests, if the results are favourable or within the acceptable range set by the insurance company, you would be accepted as a standard case.

In this situation, your premium remains unchanged, and you'll be granted the coverage as initially quoted.

- Substandard Cases: Sometimes, medical test results might reveal certain health concerns. These don't necessarily bar you from getting insurance, but they can lead to a higher premium.

For example, if Sara, who occasionally smokes, undergoes a medical test that shows slightly compromised lung function, her insurance company might categorise her as a substandard case. While she would still be offered coverage, the premium would be higher than initially quoted, reflecting the increased risk the insurer perceives.

- Decline/Postponement: In certain scenarios, the results of the medical tests might reveal significant health concerns, leading the insurer to either decline the insurance application or postpone it.

Note: You should declare your health conditions to your insurance provider before buying the term plan to avoid any rejection.

Should You Buy Term Insurance Without a Medical Test?

There's an undeniable allure to opt for life insurance without the 'perceived' hurdle of medical tests. Here's why many find this option appealing:

- Ease of Obtaining: Undoubtedly, getting term insurance without medical tests offers a swift route. Without the requirement to schedule and undergo medical examinations, the efforts required on your part are certainly minimised.

- Sidestepping Premium Hikes: If you're wary of potential pre-existing health conditions, forgoing a medical test might appear as a strategic move to keep the insurance premiums from skyrocketing.

With that said, there are some disadvantages of obtaining term insurance without a medical test as well. Here are the major points related to the disadvantages -

- Potential for Rejected Claims: By sidestepping medical evaluations, there's a risk of policy nullification. If a policyholder passes away from a pre-existing condition not disclosed during the policy purchase, insurance providers may have grounds to reject the claim.

- Comprehensive Protection of Plans with Medical Tests: The essence of life insurance lies in its capacity to shield the policyholder’s loved ones from financial uncertainties in their absence. While medical tests might momentarily influence policy costs, they ensure that the coverage offered aligns with the protection that you envision for your family.

- Diminished Scope for Tailored Policies by Underwriters: Underwriters craft insurance plans, taking into account an individual's health profile and financial needs. A medical test thus becomes an integral part of this equation, ensuring that the policy mirrors your unique circumstances and provides the desired coverage. With a term insurance plan without a medical test, however, this is usually not possible.

Bottom Line

The realm of term insurance operates on a delicate balance of risk and assurance, with medical tests becoming a focal point. A policyholder's age and the sum that they wish to assure are pivotal in determining the necessity of these medical evaluations.

Further simplifying the landscape is the availability of diverse term plans, each designed to cater to distinct requirements and preferences. From pre-written to underwritten policies, the choices are multifaceted and provide potential policyholders with a spectrum of options.

Making an informed decision, therefore, isn't just about understanding the financial implications but also about recognising the intertwined role of medical assessments in shaping those outcomes.

More From Term Insurance

Recents ArticlesPopular Articles

Best Term Insurance Plans for Self-Employed in UAE – Secure Your Future

Best Term Insurance Plans for Self-Employed in UAE – Secure Your Future Zurich Futura Whole Life Insurance – Benefits, Features & Coverage in UAE

Zurich Futura Whole Life Insurance – Benefits, Features & Coverage in UAEDiscover Zurich Futura Whole Life Insurance in the UAE. Get lifelong coverage, flexible benefits, and investment growth. Learn about policy features, optional riders, and how to apply today!

Best Life Insurance Companies in the UAE – Compare & Choose the Right Policy

Best Life Insurance Companies in the UAE – Compare & Choose the Right PolicyLooking for the best life insurance companies in the UAE? Compare top insurers, coverage options, and claim settlement ratios to secure your family’s financial future.

Term vs Whole Life Insurance in UAE: Key Differences & Benefits

Term vs Whole Life Insurance in UAE: Key Differences & BenefitsCompare term and whole life insurance in the UAE. Understand key differences, benefits, costs, and which plan suits your financial goals and budget.

- Sum Insured vs Sum Assured: Key Differences & Insurance Guide

Understand the difference between sum insured vs sum assured in insurance. Learn about their meanings, key features, and how to choose the right coverage for your needs.

Takaful Emarat Life Insurance | Choose Best Takaful Emarat Life Insurance in UAE

Takaful Emarat Life Insurance | Choose Best Takaful Emarat Life Insurance in UAETakaful Emarat Life Insurance UAE - Compare & Buy Takaful Emarat Life Insurance in Dubai, UAE. Get Financial assurance for your family with a Takaful Emarat Life Insurance

Why Choose Twenty Five Year Term Life Insurance?

Why Choose Twenty Five Year Term Life Insurance?In this article, we will understand all the key details about 25 year term insurance and its usefulness.

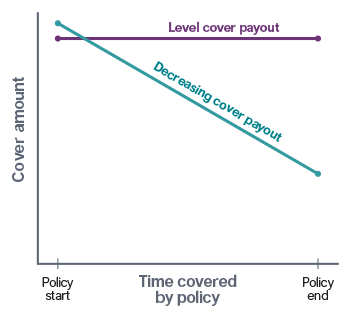

Level or Decreasing Life Insurance: What's the Difference?

Level or Decreasing Life Insurance: What's the Difference?In this article, we will explore the distinction between decreasing vs level insurance, the benefits of each type, and how you can determine what works best for you.

All You Need to Know About Level Term Life Insurance in UAE

All You Need to Know About Level Term Life Insurance in UAELet’s discuss the distinctive properties of level term insurance and its benefits. We will also understand the level term life insurance rates so that you make an informed decision!

10 Crore Life Insurance Policy - A Complete Guide

10 Crore Life Insurance Policy - A Complete GuideA 10 crore life insurance policy offers extensive coverage. It ensures the financial well-being of the family and allows them to maintain their lifestyle and meet their financial goals even in the policyholder’s absence.

- What is Surrender Value in Insurance?

Surrender value in insurance is the amount of money a policyholder receives if they cancel their policy before it matures. Check two main types of surrender values - Guaranteed Surrender Value and Special Surrender Value.

- Term Insurance Premium Calculator - A Complete Guide

Term insurance premium calculator in the UAE offers numerous advantages, streamlining the process of selecting the most suitable term insurance plan.

- Term Insurance with Return of Premium - How Does It Work?

Term insurance with return of premium – Learn about what this type of insurance is, how it works, and whether or not it’s right for you.

Who Should Be Your Nominee for Your Term Insurance?

Who Should Be Your Nominee for Your Term Insurance?We will explore into the nuances of term insurance, elucidating the meaning of the insurance nominee meaning, life insurance nominee rules, and much more.

Understanding the Slide of Decreasing Term Insurance

Understanding the Slide of Decreasing Term InsuranceWe will explore the nuances of the decreasing term life insurance plan, highlighting its salient features, benefits, and more.

Deciphering the Pros and Cons of a Term Insurance Policy

Deciphering the Pros and Cons of a Term Insurance PolicyDiscover the reasons to consider a term insurance policy. This guide provides all the information you need to make an informed decision.

How Important Is Term Insurance for Non-Working Spouses in India?

How Important Is Term Insurance for Non-Working Spouses in India?If you're married and your spouse doesn't work, explore the responsibilities and contributions of a non-working spouse, while often underestimated, are foundational to a household's functioning.

Critical Illness Riders - A Comprehensive Guide

Critical Illness Riders - A Comprehensive GuideLearn about Critical Illness Riders, a comprehensive guide that will help you navigate the unique challenges of illness.

Is It Wise to Purchase a Term Plan with Maturity Benefits?

Is It Wise to Purchase a Term Plan with Maturity Benefits?Check out our term plans with maturity benefits - these options offer you the security and stability you're searching for!